The first federal judge to consider the question concludes that compliance with Reg F does not guarantee compliance with the FDCPA.

The first federal judge to consider the question concludes that compliance with Reg F does not guarantee compliance with the FDCPA.

The first federal judge to consider the question concludes that compliance with Reg F does not guarantee compliance with the FDCPA.

The first federal judge to consider the question concludes that compliance with Reg F does not guarantee compliance with the FDCPA.02/14/2023 11:30 P.M.

9 minute read

On Feb. 9, 2023, in the first substantive decision about the scope of the safe harbor provided under Regulation F for debt collectors using the Consumer Financial Protection Bureau’s model validation notice (MVN), a judge in the U.S. District Court for the Southern District of Florida appears to have decided that the MVN safe harbor provides nearly no cover from consumers’ claims.

The decision in Roger v. GC Services, L.P. came in response to the defendant’s motion to dismiss. The defendant argued that its validation notice conformed “exactly” to the MVN as published in the CFPB’s final rule and therefore enjoyed the “information and form” safe harbor afforded under Reg F at 1006.34(d)(2).

The Complaint

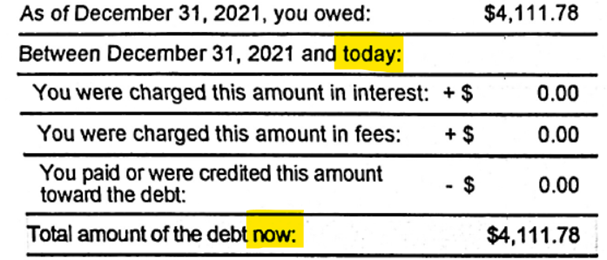

The complaint alleged that the collection agency had sent the consumer an undated validation notice that included the itemization table exactly as published in the CFPB’s final rule. That table includes a reference to “today” above the lines itemizing any interest and fees that had been added to the debt (or credits subtracted from it) since the itemization date and a reference to the total amount of the debt “now.”

The image below (with ACA’s highlighting added over the terms “today” and “now”) shows the itemization table as it appeared in the validation notice attached to the plaintiff’s complaint:

Notably, the itemization table showed that no interest, no fees and no payments or credits had accrued between the itemization date (Dec. 31, 2021) and “today” or “now.”

The plaintiff complained that the absence of a date on the letter (other than the itemization date) made it impossible to determine the date to which the terms “today” and “now” refer. As a result, the plaintiff alleged, the absence of a date on the letter that could be used to define “today” or “now” constituted withholding of a “material term” and made the letter seem “illegitimate,” “suspicious” and “misleading.”

Thus, the plaintiff alleged violations of FDCPA Sections 806 [15 U.S.C. 1692d] relating to harassment, oppression, and abuse of a consumer; 807 [1692e], relating to false or misleading representations to a consumer; 808 [1692f] relating to unfair debt collection practices; and 809 [1692g] relating to validation of debts.

The defendant moved to dismiss the plaintiff’s complaint, arguing that its compliance with Reg F in providing the consumer with a letter that “conforms exactly” to the MVN as published by the CFPB meant that it had safe harbor under Reg F and, further, that even if it did not have a safe harbor, the FDCPA itself does not require that a letter be dated.

The 1692g Analysis

The Honorable Cecilia Altonaga, chief judge of the U.S. District Court for the Southern District of Florida, began her decision with the obvious: “Admittedly … Section 1006.34 was intended to clarify Section 1692g of the FDCPA.” (Internal punctuation and quotations omitted.) From there, however, the opinion leaps to the conclusion that compliance with the FDCPA—i.e., with the federal statute itself—does not necessarily follow from compliance with the CFPB’s implementing regulation, Reg F.

Although the plaintiff argued in its opposition to GC Services’ motion for dismissal that the court need not defer to the CFPB’s regulations under the so-called Chevron doctrine—see Chevron USA v. Natural Resources Defense Council, Inc., 467 U.S. 837 (1984)—Judge Altonaga’s opinion never engages in the two-step Chevron analysis.

Rather, the opinion leaps into uncharted waters with this statement: “The parties’ competing arguments about the validity of the CFPB’s regulations [under a Chevron analysis] largely miss the point. Plaintiff does not allege that Defendant violated any CFPB regulations; he alleges violations of the FDCPA.” (Emphasis added.)

Judge Altonaga reads Reg F’s MVN safe harbor under Section 1006.34(d)(2) as providing a compliance safety net not with respect to the validation provisions of the FDCPA itself; i.e., with 15 U.S.C. 1692g(a), but rather only with respect to “the information and form requirements of this section” (emphasis added). In short, the judge reads the Reg F MVN safe harbor as a safe harbor only as to those requirements set forth by the CFPB in Section 1006.34, not with the broader (and more ambiguous) requirements set forth by Congress in FDCPA Section 809 [1692g].

In other words, in Judge Altonaga’s view, “the safe harbor Defendant relies on is created by a regulation which explicitly states it only provides coverage for regulatory—not statutory—compliance … [and] Defendant identifies no authority, within the regulation or otherwise, for its assertion that this limited regulatory safe harbor was also intended to be a broader statutory one.”

Additionally, Judge Altonaga concluded that even if the MVN safe harbor applies to some of Section 1692g’s statutory requirements, “a safe harbor for the form of provided information is different from a safe harbor for the substance of that information.”

It’s worth noting that this analysis reads out of the regulation from the CFPB’s language promising that the MVN will yield a safe harbor with respect to not only the “form” of the information provided under Section 1006.34(c) but also with respect to the “information” provided pursuant to that subsection. See Reg F at Section 1006.34(d)(2)(i) (emphasis added).

If the CFPB implemented Section 1006.34 to interpret the requirements of Section 1692g and promised that using the MVN to do so would yield a safe harbor not only with respect to the “form” in which the FDCPA-required validation information would be provided to the consumer but also as to the “information” that must be provided, then omitting the date of the letter could not reasonably be construed to be omitting required information. (Remember that the CFPB’s MVN includes no date, although an official comment to Section 1006.34(d)(2)(iii), interpreting the meaning of “substantially similar form,” allows that adding “the date the form [MVN] is generated” will yield a “substantially similar” MVN to the one published in Reg F at Model Form B-1.)

The Sections 1692e and 1692f Analyses

With respect to the Sections 1692e and 1692f claims, Judge Altonaga concluded simply that “a regulation prescribing additional requirements under 1694g [sic] has little, if anything, to say about the separate statutory requirements of Sections 1692d, 1692e, or 1692f.”

And while that’s true, if the plaintiff’s alleged violations of Sections 1692e and 1692f do in fact constitute plausible claims for relief under the FDCPA, then Judge Altonaga’s conclusion in that regard logically implies that the CFPB itself wrote a regulation and promulgated a model notice the sending of which constitutes a misleading or unfair communication with the consumer and an unfair or abusive collection practice. (Again, the MVN itself is undated and “the date the form is generated” is optional information not required by Section 1006.34(c).)

The Dating Game?

Judge Altonaga notes, based on other legal decisions, that “strict compliance with the FDCPA’s mandate that a debt collector’s initial communications state ‘the amount of the debt is often impossible, especially where variable interest and other items accrue day to day. And [e]ven if the statement is accurate when the letter is drafted and sent, it may not be accurate by the time it is received.”

Nevertheless, in Judge Altonaga’s view, “the undated letter here could easily be interpreted by a reasonable consumer, let alone the least sophisticated consumer … as not stating the full amount of the debt” because although it lists the amount due on the itemization date and the amounts that have accrued since then—no interest, no fees, and no payments or credits, meaning the itemization balance had not changed—“the letter does not contain information Defendant relied on to reach this conclusion.”

In other words, in Judge Altonaga’s view, even if the MVN showed “the amount of the debt had not yet been altered, the Letter provides no means by which Plaintiff might assess whether, and by how much, the debt might increase in the future if he did not promptly pay Defendant.”

Essentially, with this statement, it feels as though the court here has suggested a “static debt” disclosure for the MVN– almost an anti-Avila notice—when debt collectors send an undated MVN for a static debt given that, in her words, “even a careful reading of the Letter does not reveal whether, and by how much, the debt might increase.” (Never mind that neither the FDCPA nor Reg F expressly require such a disclosure.)

According to Judge Altonaga’s analysis, then, “[a]t bottom, the Letter makes multiple references to a timeline against which Defendant assessed the debt, including interest and fees … [b]ut the Letter provides no date or corresponding information, aside from the initial date when the debt was incurred …” Thus, in Judge Altonaga’s view, “the undated Letter might plausibly mislead the least-sophisticated consumer with regard to the outstanding amount of the debt.” (Cleaned up.)

Again, this analysis misses the forest for the trees: After nearly a decade of weighing its options, in 2020 the CFPB finally promulgated a long-awaited rule to, among other things, “clarify the information that a debt collector must provide to a consumer at the outset of debt collection and to provide a model notice containing the information required by FDCPA Section 809(a) [1692g(a)].” See Debt Collection Practices (Regulation F), 85 Fed. Reg. 76734, 76735 (Nov. 30, 2020) (Section I.B, “Disclosure Focused Final Rule,” not to be codified).

And, sure enough, just two months later, the bureau did what it said and released a final rule “to implement and interpret FDCPA section 809(a) and pursuant to its authority under FDCPA section 814(d) to prescribe rules with respect to the collection of debts by debt collectors.” See Debt Collection Practices (Regulation F), 86 Fed. Reg. 5766, 5819 (Jan. 19, 2021) (Section-by-Section Analysis discussing “34(d) Form of Validation Information,” not to be codified) (emphasis added).

Thus, to conclude that Reg F’s MVN safe harbor does not directly tie to the CFPB’s implementation and interpretation of the lacking standard mentioned in FDCPA Section 809(a) [1692g(a)] misses the entire point of the bureau’s December 2020 final rule.

The 1692d Claim

Mercifully, this analysis did not extend to the plaintiff’s 1692d claim, meaning that in Judge Altonaga’s view, the undated MVN does not amount to “harassment, oppression, or abuse” under the FDCPA. But the dismissal of this portion of the plaintiff’s claim relies largely on his failure to address the applicable standard under Jeter v. Credit Bureau, Inc., 760 F.2d 1168, 1179 (11th Cir. 1985) and his failure to provide in his complaint “information to determine whether [he] is a consumer whose circumstances make him relatively more susceptible to harassment, oppression, or abuse.” (Internal quotations omitted and cleaned up.)

ACA’s Take

It’s unclear what ultimately will happen with the plaintiff’s claims in Roger v. GC Services, as they have largely survived a motion to dismiss but have not yet been tested through a motion for summary judgment.

At the same time, as many industry attorneys have counseled, it appears to remain a best practice—if not squarely required by either Reg F or the FDCPA—to put a date on your validation letters even if you’re using a near-exact copy of the undated Model Validation Notice published by the CFPB itself at Regulation F, Model Form B-1.

If you have executive leadership updates or other member news to share with ACA, contact our communications department at [email protected]. View our publications page for more information and our news submission guidelines here.

![]()

![]()

![]()

![]()

![]()